Blockchain Technology Most Details

What Is Blockchain Technology?

Blockchain is a method of recording information that makes it impossible or difficult for the system to be changed, hacked, or manipulated. A blockchain is a distributed ledger that duplicates and distributes transactions across the network of computers participating in the blockchain.

Blockchain technology is a structure that stores transactional records, also known as the block, of the public in several databases, known as the “chain,” in a network connected through peer-to-peer nodes. Typically, this storage is referred to as a ‘digital ledger.’

Every transaction in this ledger is authorized by the digital signature of the owner, which authenticates the transaction and safeguards it from tampering. Hence, the information the digital ledger contains is highly secure.

In simpler words, the digital ledger is like a Google spreadsheet shared among numerous computers in a network, in which, the transactional records are stored based on actual purchases. The fascinating angle is that anybody can see the data, but they can’t corrupt it.

Why is Blockchain Popular?

Suppose you are transferring money to your family or friends from your bank account. You would log in to online banking and transfer the amount to the other person using their account number. When the transaction is done, your bank updates the transaction records. It seems simple enough, right? There is a potential issue which most of us neglect.

These types of transactions can be tampered with very quickly. People who are familiar with this truth are often wary of using these types of transactions, hence the evolution of third-party payment applications in recent years. But this vulnerability is essentially why Blockchain technology was created.

Technologically, Blockchain is a digital ledger that is gaining a lot of attention and traction recently. But why has it become so popular? Well, let’s dig into it to fathom the whole concept.

Record keeping of data and transactions are a crucial part of the business. Often, this information is handled in house or passed through a third party like brokers, bankers, or lawyers increasing time, cost, or both on the business. Fortunately, Blockchain avoids this long process and facilitates the faster movement of the transaction, thereby saving both time and money.

Most people assume Blockchain and Bitcoin can be used interchangeably, but in reality, that’s not the case. Blockchain is the technology capable of supporting various applications related to multiple industries like finance, supply chain, manufacturing, etc., but Bitcoin is a currency that relies on Blockchain technology to be secure.

Blockchain is an emerging technology with many advantages in an increasingly digital world:

Highly Secure

It uses a digital signature feature to conduct fraud-free transactions making it impossible to corrupt or change the data of an individual by the other users without a specific digital signature.Decentralized System

Conventionally, you need the approval of regulatory authorities like a government or bank for transactions; however, with Blockchain, transactions are done with the mutual consensus of users resulting in smoother, safer, and faster transactions.Automation Capability

It is programmable and can generate systematic actions, events, and payments automatically when the criteria of the trigger are met.

How Does Blockchain Technology Work?

In recent years, you may have noticed many businesses around the world integrating Blockchain technology. But how exactly does Blockchain technology work? Is this a significant change or a simple addition? The advancements of Blockchain are still young and have the potential to be revolutionary in the future; so, let’s begin demystifying this technology.

Blockchain is a combination of three leading technologies:

- Cryptographic keys

- A peer-to-peer network containing a shared ledger

- A means of computing, to store the transactions and records of the network

Cryptography keys consist of two keys – Private key and Public key. These keys help in performing successful transactions between two parties. Each individual has these two keys, which they use to produce a secure digital identity reference. This secured identity is the most important aspect of Blockchain technology. In the world of cryptocurrency, this identity is referred to as ‘digital signature’ and is used for authorizing and controlling transactions.

The digital signature is merged with the peer-to-peer network; a large number of individuals who act as authorities use the digital signature in order to reach a consensus on transactions, among other issues. When they authorize a deal, it is certified by a mathematical verification, which results in a successful secured transaction between the two network-connected parties. So to sum it up, Blockchain users employ cryptography keys to perform different types of digital interactions over the peer-to-peer network.

Types of Blockchain

There are four different types of blockchains. They are as follows:

Private Blockchain Networks

Private blockchains operate on closed networks, and tend to work well for private businesses and organizations. Companies can use private blockchains to customize their accessibility and authorization preferences, parameters to the network, and other important security options. Only one authority manages a private blockchain network.

Public Blockchain Networks

Bitcoin and other cryptocurrencies originated from public blockchains, which also played a role in popularizing distributed ledger technology (DLT). Public blockchains also help to eliminate certain challenges and issues, such as security flaws and centralization. With DLT, data is distributed across a peer-to-peer network, rather than being stored in a single location. A consensus algorithm is used for verifying information authenticity; proof of stake (PoS) and proof of work (PoW) are two frequently used consensus methods.

Permissioned Blockchain Networks

Also sometimes known as hybrid blockchains, permissioned blockchain networks are private blockchains that allow special access for authorized individuals. Organizations typically set up these types of blockchains to get the best of both worlds, and it enables better structure when assigning who can participate in the network and in what transactions.

Consortium Blockchains

Similar to permissioned blockchains, consortium blockchains have both public and private components, except multiple organizations will manage a single consortium blockchain network. Although these types of blockchains can initially be more complex to set up, once they are running, they can offer better security. Additionally, consortium blockchains are optimal for collaboration with multiple organizations.

The Process of Transaction

One of Blockchain technology’s cardinal features is the way it confirms and authorizes transactions. For example, if two individuals wish to perform a transaction with a private and public key, respectively, the first person party would attach the transaction information to the public key of the second party. This total information is gathered together into a block.

The block contains a digital signature, a timestamp, and other important, relevant information. It should be noted that the block doesn’t include the identities of the individuals involved in the transaction. This block is then transmitted across all of the network's nodes, and when the right individual uses his private key and matches it with the block, the transaction gets completed successfully.

In addition to conducting financial transactions, the Blockchain can also hold transactional details of properties, vehicles, etc.

Here’s a use case that illustrates how Blockchain works:

Hash Encryptions

blockchain technology uses hashing and encryption to secure the data, relying mainly on the SHA256 algorithm to secure the information. The address of the sender (public key), the receiver’s address, the transaction, and his/her private key details are transmitted via the SHA256 algorithm. The encrypted information, called hash encryption, is transmitted across the world and added to the blockchain after verification. The SHA256 algorithm makes it almost impossible to hack the hash encryption, which in turn simplifies the sender and receiver’s authentication.Proof of Work

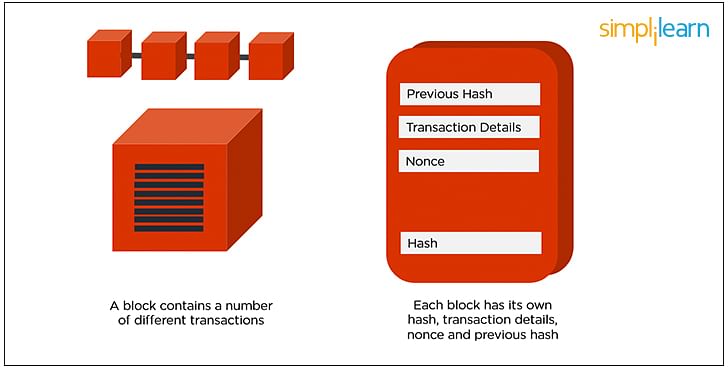

In a Blockchain, each block consists of 4 main headers.- Previous Hash: This hash address locates the previous block.

- Transaction Details: Details of all the transactions that need to occur.

- Nonce: An arbitrary number given in cryptography to differentiate the block’s hash address.

- Hash Address of the Block: All of the above (i.e., preceding hash, transaction details, and nonce) are transmitted through a hashing algorithm. This gives an output containing a 256-bit, 64 character length value, which is called the unique ‘hash address.’ Consequently, it is referred to as the hash of the block.

- Numerous people around the world try to figure out the right hash value to meet a pre-determined condition using computational algorithms. The transaction completes when the predetermined condition is met. To put it more plainly, Blockchain miners attempt to solve a mathematical puzzle, which is referred to as a proof of work problem. Whoever solves it first gets a reward.

Mining

In Blockchain technology, the process of adding transactional details to the present digital/public ledger is called ‘mining.’ Though the term is associated with Bitcoin, it is used to refer to other Blockchain technologies as well. Mining involves generating the hash of a block transaction, which is tough to forge, thereby ensuring the safety of the entire Blockchain without needing a central system.

Over the past few years, you have consistently heard the term ‘blockchain technology,’ probably regarding cryptocurrencies, like Bitcoin. In fact, you may be asking yourself, “what is blockchain technology?” It seems like blockchain is a platitude but in a hypothetical sense, as there is no real meaning that the layman can understand easily. It is imperative to answer “what is blockchain technology, “including the technology that is used, how it works, and how it’s becoming vital in the digital world.

As blockchain continues to grow and become more user-friendly, the onus is on you to learn this evolving technology to prepare for the future. If you are new to blockchain, then this is the right platform to gain solid foundational knowledge. In this article, you learn how to answer the question, “what is blockchain technology?” You’ll also learn how blockchain works, why it’s important, and how you can use this field to advance your career.

What Is Blockchain Technology?

Blockchain is a method of recording information that makes it impossible or difficult for the system to be changed, hacked, or manipulated. A blockchain is a distributed ledger that duplicates and distributes transactions across the network of computers participating in the blockchain.

Blockchain technology is a structure that stores transactional records, also known as the block, of the public in several databases, known as the “chain,” in a network connected through peer-to-peer nodes. Typically, this storage is referred to as a ‘digital ledger.’

Every transaction in this ledger is authorized by the digital signature of the owner, which authenticates the transaction and safeguards it from tampering. Hence, the information the digital ledger contains is highly secure.

In simpler words, the digital ledger is like a Google spreadsheet shared among numerous computers in a network, in which, the transactional records are stored based on actual purchases. The fascinating angle is that anybody can see the data, but they can’t corrupt it.

Why is Blockchain Popular?

Suppose you are transferring money to your family or friends from your bank account. You would log in to online banking and transfer the amount to the other person using their account number. When the transaction is done, your bank updates the transaction records. It seems simple enough, right? There is a potential issue which most of us neglect.

These types of transactions can be tampered with very quickly. People who are familiar with this truth are often wary of using these types of transactions, hence the evolution of third-party payment applications in recent years. But this vulnerability is essentially why Blockchain technology was created.

Technologically, Blockchain is a digital ledger that is gaining a lot of attention and traction recently. But why has it become so popular? Well, let’s dig into it to fathom the whole concept.

Record keeping of data and transactions are a crucial part of the business. Often, this information is handled in house or passed through a third party like brokers, bankers, or lawyers increasing time, cost, or both on the business. Fortunately, Blockchain avoids this long process and facilitates the faster movement of the transaction, thereby saving both time and money.

Most people assume Blockchain and Bitcoin can be used interchangeably, but in reality, that’s not the case. Blockchain is the technology capable of supporting various applications related to multiple industries like finance, supply chain, manufacturing, etc., but Bitcoin is a currency that relies on Blockchain technology to be secure.

Blockchain is an emerging technology with many advantages in an increasingly digital world:

Highly Secure

It uses a digital signature feature to conduct fraud-free transactions making it impossible to corrupt or change the data of an individual by the other users without a specific digital signature.Decentralized System

Conventionally, you need the approval of regulatory authorities like a government or bank for transactions; however, with Blockchain, transactions are done with the mutual consensus of users resulting in smoother, safer, and faster transactions.Automation Capability

It is programmable and can generate systematic actions, events, and payments automatically when the criteria of the trigger are met.

How Does Blockchain Technology Work?

In recent years, you may have noticed many businesses around the world integrating Blockchain technology. But how exactly does Blockchain technology work? Is this a significant change or a simple addition? The advancements of Blockchain are still young and have the potential to be revolutionary in the future; so, let’s begin demystifying this technology.

Blockchain is a combination of three leading technologies:

- Cryptographic keys

- A peer-to-peer network containing a shared ledger

- A means of computing, to store the transactions and records of the network

Cryptography keys consist of two keys – Private key and Public key. These keys help in performing successful transactions between two parties. Each individual has these two keys, which they use to produce a secure digital identity reference. This secured identity is the most important aspect of Blockchain technology. In the world of cryptocurrency, this identity is referred to as ‘digital signature’ and is used for authorizing and controlling transactions.

The digital signature is merged with the peer-to-peer network; a large number of individuals who act as authorities use the digital signature in order to reach a consensus on transactions, among other issues. When they authorize a deal, it is certified by a mathematical verification, which results in a successful secured transaction between the two network-connected parties. So to sum it up, Blockchain users employ cryptography keys to perform different types of digital interactions over the peer-to-peer network.

Types of Blockchain

There are four different types of blockchains. They are as follows:

Private Blockchain Networks

Private blockchains operate on closed networks, and tend to work well for private businesses and organizations. Companies can use private blockchains to customize their accessibility and authorization preferences, parameters to the network, and other important security options. Only one authority manages a private blockchain network.

Public Blockchain Networks

Bitcoin and other cryptocurrencies originated from public blockchains, which also played a role in popularizing distributed ledger technology (DLT). Public blockchains also help to eliminate certain challenges and issues, such as security flaws and centralization. With DLT, data is distributed across a peer-to-peer network, rather than being stored in a single location. A consensus algorithm is used for verifying information authenticity; proof of stake (PoS) and proof of work (PoW) are two frequently used consensus methods.

Permissioned Blockchain Networks

Also sometimes known as hybrid blockchains, permissioned blockchain networks are private blockchains that allow special access for authorized individuals. Organizations typically set up these types of blockchains to get the best of both worlds, and it enables better structure when assigning who can participate in the network and in what transactions.

Consortium Blockchains

Similar to permissioned blockchains, consortium blockchains have both public and private components, except multiple organizations will manage a single consortium blockchain network. Although these types of blockchains can initially be more complex to set up, once they are running, they can offer better security. Additionally, consortium blockchains are optimal for collaboration with multiple organizations.

The Process of Transaction

One of Blockchain technology’s cardinal features is the way it confirms and authorizes transactions. For example, if two individuals wish to perform a transaction with a private and public key, respectively, the first person party would attach the transaction information to the public key of the second party. This total information is gathered together into a block.

The block contains a digital signature, a timestamp, and other important, relevant information. It should be noted that the block doesn’t include the identities of the individuals involved in the transaction. This block is then transmitted across all of the network's nodes, and when the right individual uses his private key and matches it with the block, the transaction gets completed successfully.

In addition to conducting financial transactions, the Blockchain can also hold transactional details of properties, vehicles, etc.

Here’s a use case that illustrates how Blockchain works:

Hash Encryptions

blockchain technology uses hashing and encryption to secure the data, relying mainly on the SHA256 algorithm to secure the information. The address of the sender (public key), the receiver’s address, the transaction, and his/her private key details are transmitted via the SHA256 algorithm. The encrypted information, called hash encryption, is transmitted across the world and added to the blockchain after verification. The SHA256 algorithm makes it almost impossible to hack the hash encryption, which in turn simplifies the sender and receiver’s authentication.Proof of Work

In a Blockchain, each block consists of 4 main headers.- Previous Hash: This hash address locates the previous block.

- Transaction Details: Details of all the transactions that need to occur.

- Nonce: An arbitrary number given in cryptography to differentiate the block’s hash address.

- Hash Address of the Block: All of the above (i.e., preceding hash, transaction details, and nonce) are transmitted through a hashing algorithm. This gives an output containing a 256-bit, 64 character length value, which is called the unique ‘hash address.’ Consequently, it is referred to as the hash of the block.

- Numerous people around the world try to figure out the right hash value to meet a pre-determined condition using computational algorithms. The transaction completes when the predetermined condition is met. To put it more plainly, Blockchain miners attempt to solve a mathematical puzzle, which is referred to as a proof of work problem. Whoever solves it first gets a reward.

Mining

In Blockchain technology, the process of adding transactional details to the present digital/public ledger is called ‘mining.’ Though the term is associated with Bitcoin, it is used to refer to other Blockchain technologies as well. Mining involves generating the hash of a block transaction, which is tough to forge, thereby ensuring the safety of the entire Blockchain without needing a central system.

History of Blockchain

Satoshi Nakamoto, whose real identity still remains unknown to date, first introduced the concept of blockchains in 2008. The design continued to improve and evolve, with Nakamoto using a Hashcash-like method. It eventually became a primary component of bitcoin, a popular form of cryptocurrency, where it serves as a public ledger for all network transactions. Bitcoin blockchain file sizes, which contained all transactions and records on the network, continued to grow substantially. By August 2014, it had reached 20 gigabytes, and eventually exceeded 200 gigabytes by early 2020.

Advantages and Disadvantages of Blockchain

Like all forms of technology, blockchain has several advantages and disadvantages to consider.

Advantages

One major advantage of blockchains is the level of security it can provide, and this also means that blockchains can protect and secure sensitive data from online transactions. For anyone looking for speedy and convenient transactions, blockchain technology offers this as well. In fact, it only takes a few minutes, whereas other transaction methods can take several days to complete. There is also no third-party interference from financial institutions or government organizations, which many users look at as an advantage.

Disadvantages

Blockchain and cryptography involves the use of public and private keys, and reportedly, there have been problems with private keys. If a user loses their private key, they face numerous challenges, making this one disadvantage of blockchains. Another disadvantage is the scalability restrictions, as the number of transactions per node is limited. Because of this, it can take several hours to finish multiple transactions and other tasks. It can also be difficult to change or add information after it is recorded, which is another significant disadvantage of blockchain.

How Is Blockchain Used?

Blockchains store information on monetary transactions using cryptocurrencies, but they also store other types of information, such as product tracking and other data. For example, food products can be tracked from the moment they are shipped out, all throughout their journey, and up until final delivery. This information can be helpful because if there is a contamination outbreak, the source of the outbreak can be easily traced. This is just one of the many ways that blockchains can store important data for organizations.

How to Invest in Blockchain Technology

Blockchain technology and stocks can be a lucrative investment, and there are several ways to take the next step toward making your first blockchain investment purchase. Bitcoin is typically the first thing that comes to mind when it comes to investing in blockchain technology, and it shouldn’t be overlooked. Aside from Bitcoin, there is also the option of investing in cryptocurrency penny stocks, such as Altcoin and Litecoin. There are also certain apps and services that are in the pre-development phase and that are using blockchain technology to raise funding. As an investor, you can buy coins, with the expectation that prices will go up if the service or app becomes popular. Another way to invest in blockchain technology is to invest in startups built on blockchain technology. Finally, there is always the option to invest in pure blockchain technology.

What Are the Implications of Blockchain Technology?

Blockchain technology has made a great impact on society, including:

- Bitcoin, Blockchain’s prime application and the whole reason the technology was developed in the first place, has helped many people through financial services such as digital wallets. It has provided microloans and allowed micropayments to people in less than ideal economic circumstances, thereby introducing new life in the world economy.

- The next major impact is in the concept of TRUST, especially within the sphere of international transactions. Previously, lawyers were hired to bridge the trust gap between two different parties, but it consumed extra time and money. But the introduction of Cryptocurrency has radically changed the trust equation. Many organizations are located in areas where resources are scarce, and corruption is widespread. In such cases, Blockchain renders a significant advantage to these affected people and organizations, allowing them to escape the tricks of unreliable third-party intermediaries.

- The new reality of the Internet of Things (IoT) is already teeming with smart devices that — turn on your washing machines; drive your cars; navigate your ships; organize trash pick-up; manage traffic safety in your community — you name it! This is where blockchain comes in. In all of these cases (and more), leveraging blockchain technology by creating Smart Contracts will enable any organization to ‒ both — improve operations and keep more accurate records.

- Blockchain technology enables a decentralized peer-to-peer network for organizations or apps like Airbnb and Uber. It allows people to pay for things like toll fees, parking, etc.

- Blockchain technology can be used as a secure platform for the healthcare industry for the purposes of storing sensitive patient data. Health-related organizations can create a centralized database with the technology and share the information with only the appropriately authorized people.

- In the private consumer world, blockchain technology can be employed by two parties who wish to conduct a private transaction. However, these kinds of transactions have details that need to be hammered out before both parties can proceed:

- What are the terms and conditions (T&C) of the exchange?

- Are all the terms clear?

- When does the exchange start?

- When will it finish?

- When is it unfair to halt the exchange?

Since blockchain technology employs a shared ledger, distributed ledger on a decentralized network, all parties involved can quickly find answers to these questions by researching “blocks” in the “chain.” Transactions on a blockchain platform can be tracked from departure to the destination by all of the transactions on the chain.

Comments